How to Choose the Right Buyer for Your Security Company

Who Gets the Songs: Choosing the Right Buyer for Your Security Company

Bob Dylan sold his life's work. So did Springsteen. The price made the headlines. The decision they actually agonized over was who.

I've been watching musicians sell their lives.

In December 2020, Bob Dylan sold his entire songwriting catalog — some six hundred songs, sixty years of work — to Universal for a reported sum north of $300 million. A year later Bruce Springsteen sold his catalog to Sony for a figure widely reported around half a billion dollars. After that the floodgates opened. Neil Young. Stevie Nicks. Half the Rock and Roll Hall of Fame, it seemed, cashing in the songbook.

The headlines were always the number. The number is easy to write about.

But the number was never the hard part. For an artist with that kind of catalog, the price was always going to be enormous. The decision that kept them up at night was the other one. Who gets to own the songs. Who decides where "Born to Run" plays for the next fifty years. Who they hand sixty years of work to.

I run NextGen Live Security, a HoldCo building a platform across the security industry. So I didn't read those deals as entertainment news. I read them as the cleanest case study I've found for an owner thinking about selling a company. Because if you own a security business, you own a catalog. And one day, you will choose who gets the songs.

Here is the part nobody tells you: the price is a number you negotiate once. The buyer is a decision you live inside for a decade.

This is for the owner of a security company — guarding, alarm, monitoring, integration — who is starting to think about an exit, and wants to think clearly about who should be sitting on the other side of the table.

Your Company Is a Catalog, Not a Job.

A songwriter spends thirty years working and ends up with a catalog — a body of work that throws off royalties whether or not he ever writes another line. The catalog is an asset. It exists independent of the man.

Most security owners never quite make that mental move.

They run the company as a job. A very good job, one that pays them well every year. The paycheck is real, and it feels like the point. But the paycheck quietly hides the thing that actually matters.

Your company is a catalog. Every contract you've signed, every account that renews on the first of the month, every block of recurring monthly revenue, every relationship with a property manager or a general contractor or the local fire marshal — each one is a song in the catalog. Together they have a value that exists separate from the salary you draw.

The day you decide to sell, you stop being the songwriter and become the owner of a catalog choosing its next custodian. The whole game changes.

Why this matters if you own a security company: until you see the catalog, you'll evaluate buyers the way a man compares paychecks — biggest number wins. Once you see the catalog, you start asking the question that actually decides your next decade. Who should own the songs, and what will they do with them.

Key Insight — Map vs. Territory. The salary you draw is the map of your company's worth. The catalog — the contracted, recurring, transferable cash flow, and the trust underneath it — is the territory. Spend a whole career reading only the map and you'll misjudge the territory the one time it truly counts.

The Major Label Will Pay the Most — and Take Your Name Off the Door.

When a major label buys a catalog, it pays top dollar. It can afford to, because it can do things with those songs you never could — sync them into films, bundle them, push them through a global machine. The industry word for that is synergy.

In your world, the major label is the strategic buyer. A larger competitor. An adjacent player — a guarding firm buying your alarm book, an integrator buying your monitoring operation. They can pay the highest headline number because your overhead becomes their savings. They close fast. They already understand the industry, so diligence is shorter.

That is the real, honest case for a strategic sale. Now understand what synergy means in plain English.

It means your back office is redundant.

It means the name on your trucks gets repainted inside eighteen months.

It means your longest-tenured people — the ones who built this with you — are precisely the ones the buyer's model is quietly counting on letting go. That is not cruelty. It is arithmetic. It is the synergy they paid you for.

And if the deal carries an earnout, a strategic buyer often ties it to integration outcomes — cross-sell targets, retention metrics — that you no longer control the morning after closing.

Why this matters: a strategic sale can be exactly the right move. If your single, honest priority is the highest possible number and a clean walk-away, you should welcome strategic buyers into a competitive process and chase that number hard. Just walk in clear-eyed about the trade. You are selling the catalog to someone who bought it to absorb it — not to keep it singing under your name.

Key Insight — Second-Order Thinking. The first-order result of a strategic sale is the biggest check. The second-order results — the name, the team, the customers, your reputation in a town where everyone knows you — are the ones you will actually live with. Negotiate the second-order terms as hard as you negotiate the first-order price.

The Fund Buys the Catalog to Sell the Catalog.

A lot of the catalog buyers in that gold rush weren't labels at all. They were funds.

The most famous, Hipgnosis, raised enormous capital and bought songs aggressively, treating catalogs as a financial asset class to be assembled and traded. For a while it looked unstoppable. Then came the hard part — painful writedowns, restless investors, and ultimately the fund itself being sold off. A big buyer paying a big number, it turned out, is not the same thing as a buyer who was right.

Private equity is the fund. PE buys your company as a "platform" or a "tuck-in," grows it for a defined window — usually three to seven years — and then sells it again. That is not a criticism of PE. It is simply the model, and the clock is structural. They are required to sell.

The upside is genuine. PE often brings strong total consideration: a healthy slug of cash plus rollover equity. And rollover equity is your second bite — the way you keep points on the catalog so you get paid again when the fund resells the larger company.

The cautions are just as genuine. Governance tightens — board approvals, reporting thresholds, decisions that used to take you an afternoon. The team gets "optimized," because efficiency is part of the investment thesis. And you are now on someone else's clock. In five years the company sells again, whether or not the timing suits you, your customers, or your people.

Hipgnosis is the reminder worth keeping. The second bite is real upside when the platform performs. When it doesn't, the second bite is a markdown.

Key Insight — Probabilistic Thinking. Don't ask whether the second bite will pay off. Ask what the full range of outcomes is, and how likely each one is. Rollover equity can be worth several times your cash at close — or a fraction of it. Size how much you roll so that even the bad branch of that tree is a future you can comfortably live in.

The Patient Owner Never Has to Sell.

There's a quieter kind of catalog buyer. The one who buys to hold. No fund life, no countdown, no obligation to flip. It grows value the slow way — by owning well, year after year, and letting it compound.

That is a HoldCo. A permanent-capital platform. Unlike a PE fund, a HoldCo is not structurally required to resell on anyone's timeline. It can think in decades.

That one structural difference changes the behavior all the way down.

A HoldCo usually keeps your brand — because in a trust business the local name is the asset it paid for, and repainting the trucks would be lighting money on fire. It tends to invest in the team rather than thin it, because it has to live alongside that team for a very long time. And it can offer you a genuinely flexible role — stay on, transition slowly, or step out — with rollover equity that gives you a real second bite.

Now the honest objections, because a guide that only flatters one option is a brochure, not a guide.

A HoldCo is usually a smaller buyer than mega-PE, which means it will rarely win a pure, maximum-price auction. It may bring less acquisition firepower than a giant platform. And — this is the one that matters most — the model does not guarantee the operator. A HoldCo is only ever as good as the people running it.

So diligence them harder than they diligence you. Ask to speak directly with the last three founders who sold to them. Ask what happened to those teams, and those brands, three years after the check cleared. Then believe what you hear, not what's printed in the deck.

Why this matters: if your definition of a good outcome includes the people and the name, and not only the size of the wire, the patient owner is built for exactly you. But "patient capital" is a category, not a character reference. Verify the operator.

Key Insight — Incentives. Show me the incentive and I'll show you the outcome. A buyer with a five-year fund clock and a buyer with no clock at all will make honestly different decisions about your brand and your people — not because one is virtuous and the other isn't, but because they are structurally pointed in different directions. Read the structure. It will tell you more than the promises.

The Collector Wants to Play the Songs Himself.

There's a fourth buyer at the door. Not a label, not a fund, not a platform. A single person who loves the catalog enough to want to own it and play it himself.

In the business world, that's the search fund. One entrepreneur — usually backed by a group of investors — who raises capital to buy a single company and run it personally. It is the heart of what's called Entrepreneurship Through Acquisition.

The appeal is real, and it's human. This is a true successor — someone who will live inside the business, walk the floor, learn the customers by name, rather than fold it into a portfolio and a quarterly report. They usually keep the brand, the team, the local identity. They are motivated the way only an owner can be.

The cautions are just as real. The searcher operates the company, which means you, as CEO, are stepping out — not staying on. The deals tend to be smaller; many searchers simply can't stretch to a larger price tag. The financing is often SBA-heavy and can be more fragile than institutional capital. And the entire plan rides on one individual, frequently a first-time CEO, carrying the weight of your life's work.

Why this matters: a search fund can be a genuinely beautiful outcome for a smaller company whose owner is truly ready to hand over the keys. Just underwrite the human being as carefully as that human being underwrites your company.

Key Insight — Single Point of Failure. A strategic, a fund, a HoldCo — each is an organization with depth behind it. A search fund is a person. That can be the warmest outcome on this entire list or the most fragile one, and the difference is, almost entirely, the individual. Diligence the operator as if the whole deal depends on them. It does.

The Headline Number Is Not the Royalty Check.

When the press reported a catalog "sold for $300 million," that is not the figure that hit the artist's account. There were structures, holdbacks, taxes, terms. There always are.

Two offers with the identical headline price can be wildly different deals. So learn the parts.

Cash at close is the money wired on closing day — the most certain dollars in the whole transaction. Rollover equity is the stake you keep in the new company — your second bite, and either your most valuable line item or your most disappointing one. A seller note is you financing part of the price yourself and getting paid over time; it bridges a valuation gap, but it parks your money behind the buyer's future performance. An earnout is a contingent payment tied to future results — and here's the line to remember: fight to tie it to financial metrics like EBITDA, which you can still influence, rather than to integration outcomes like cross-sell, which you cannot once your authority shrinks. Escrow is the slice held back against post-close claims; it's normal, but negotiate its size and its release date. And the working capital peg is the boring, technical item that quietly costs unprepared sellers six figures — make your advisor model it before you sign anything.

So never compare offers on the headline number. Compare them on risk-adjusted value: how much is certain, how realistic the earnout actually is, how credible the equity really is.

Key Insight — Margin of Safety. The gap between the headline number and the cash you can genuinely count on is your exposure. A deal that's 90% cash at close carries a wide margin of safety. A deal that's 40% cash and 60% "trust me" does not. Structure it so that even if the optimistic half never arrives, you still did just fine.

Rank Your Own List Before You Take a Single Meeting.

Here is the thing almost no owner does, and every owner should.

Before you take one buyer meeting, sit down and rank what you actually want.

Seven things usually belong on that list. The highest headline price. The certainty of the cash. Whether the brand survives. Whether your team keeps their jobs and grows. What your own role looks like the day after close. Whether there's a real, credible second bite. And whether you would be genuinely proud to have this partner's name standing next to yours in the town where you built this.

Rank them. Honestly — not how you think you should answer, how you actually feel. Then score every serious buyer against your ranking, not against each other's pitch decks.

The ranking does the work for you.

If "highest price" and "clean break" sit at the top, you are pointed straight at a competitive auction full of strategic buyers. Run one. Hire an advisor. Don't apologize for it. If "the name survives," "the team grows," and "a partner I'd be proud of" sit at the top, you are pointed at a HoldCo or a search fund — and the structure of the deal will matter as much as its size.

And there are paths I haven't dwelt on that may top your particular list — selling to your own management team, or to an employee ownership trust. Smaller headline number, usually. Maximum continuity. They belong on the list too.

Now the uncomfortable part, because an honest guide has to say it. If you read all of this and your ranking points you toward a strategic buyer and a loud, competitive auction — then that is the right answer for you, and a good advisor will tell you so even when they'd rather you picked them. The goal of this piece was never to win you. The goal is for you to choose well.

Key Insight — Inversion. Don't begin by asking which buyer is best. Begin by asking what would make this the wrong sale — the name gone, the team gutted, the cash that never showed up, the partner you grew to resent. Name the bad outcome first, in detail. Then choose the buyer least likely to deliver it.

Decide Who Gets the Songs.

Dylan didn't lose sleep over the number. Neither did Springsteen. The number was always going to be large.

What they weighed was who. Who would steward sixty years of work. Who would decide where the songs lived next, and how they'd be treated, and whose name would be attached to them long after the artist was done.

You will make the very same decision about the catalog you spent your life writing — every contract, every renewal, every hard-won relationship, every officer you trained and customer you kept. The price will get all the attention. The buyer is the part you actually live inside.

So do the unglamorous work. See the company as a catalog, not a job. Learn the four buyers and what each one is built to do. Rank your own list before anyone else hands you theirs. Read the structure, not the pitch.

For what it's worth, here is where we stand. NextGen Live Security is a HoldCo focused only on the security industry — live video monitoring and remote guarding, systems integration, access control, commercial fire and security alarms, perimeter security. We are the patient owner. No fund clock. We keep the name, we invest in the team, we build the platform around what you started, and we structure deals so you hold a real second bite.

If you want a confidential conversation about your options — no listing, no pressure, and an honest answer even when that answer is "go talk to a strategic" — that is exactly what we're here for.

You spent a lifetime writing the catalog.

Decide who gets the songs.

Remote Video Monitoring vs. Guards: Owner's Guide

The Machine in the Wall: What the Bank Teller Knows About Your Guard Company

Nobody mourns the bank teller. Banking didn't die when the machine arrived — it grew bigger, earned more, and became worth far more. It simply stopped running on people behind counters. If you own a security guard company, that is the most important story you are not thinking about.

I've been thinking about bank tellers.

Not the people. The job. Picture a bank in 1975. A lobby. A long counter. A row of windows, and behind each window a teller, counting cash by hand, one customer at a time. The bank's entire capacity to serve its town came down to a simple piece of arithmetic: how many windows were open, times how fast each teller could work.

Then somebody put a machine in the wall.

When the ATM arrived, everyone assumed it would gut the workforce and hollow out the banks. It did the opposite. Banking didn't shrink. It exploded. Banks served more customers, in more places, and made more money doing it. The machine — not the teller — became the engine. And the teller window quietly stopped being where the value lived.

I run NextGen Live Security, a HoldCo building a platform in remote video monitoring and live guarding. So I don't read the story of the bank teller as nostalgia. I read it as a forecast. Because if you own a security guard company, you are running a lobby full of teller windows.

And the machine is already in the wall.

This is for the owner who built something real — a guard company, an alarm book, a monitoring operation — over 20 or 30 years, and wants a clear-eyed answer before they exit. Not a panic. The math.

Here's the memo.

The Bank Never Sold Cash. It Sold Trust.

The teller slid you a stack of twenties, but cash was never the product.

The product was trust. Trust that your money was safe, accounted for, and there when you reached for it. The teller was just the delivery mechanism — a human face on a promise.

Sound familiar?

You have never sold guards. You sell what a guard delivers — the parking lot that stays empty, the construction site that still has its copper at sunrise, the night a business owner finally sleeps because somebody is watching. Pinkerton branded that promise in 1850 with an unblinking eye and three words: We Never Sleep. You sell the exact same thing today.

The product has not changed in 175 years.

What changed in banking was never the product. It was the machine underneath it. A teller window and an ATM deliver the identical promise. But one of them costs a salary every two weeks, turns over, trains slowly, and calls in sick. The other one does not.

Why this matters if you own a guard company: manned guarding is the teller window. Remote video monitoring is the machine in the wall. Same product — security, the end of uncertainty — built on two completely different cost structures. And the market has started paying very different prices for each.

Key Insight — First Principles. Strip the business to its core and the product is permanent: the end of the uncertainty that keeps your customer awake. Everything above that — the uniform, the truck, the teller window, the camera — is just machinery, and machinery gets replaced. The owners who fall in love with the machinery instead of the product tend to get replaced along with it.

One Teller Serves One Customer. The Machine Serves Ten Thousand.

Here is the hard ceiling of the teller window. It scales in exactly one direction: more people.

More customers means more windows, more tellers, more salaries, more turnover to manage. The teller is the capacity. The only operating leverage a branch manager ever had was orchestration — squeezing a little more throughput out of the people already on the payroll.

Guarding is identical. It scales linearly with human bodies. One post, one officer, every shift, forever. Your leverage is scheduling discipline, overtime control, route density. Real skill. Also a game with a hard ceiling, because the labor is the product.

And that labor gets more expensive and harder to hold every single year.

Contract security ran roughly 77% annual turnover in 2024, up from about 69% in 2019. Plenty of individual firms run 100% to 300% — they replace their entire workforce inside a year. More than 60% of security firms name rising hourly pay as their top turnover driver, and yet the median guard still earns around $38,000, a wage that has barely moved in real terms in two decades. You are paying more, and your officers still feel underpaid. In 2025 the Department of Labor pushed the Service Contract Act health-and-welfare fringe to $5.55 an hour — a hard, non-negotiable add to every billable hour on covered work.

That is the labor-arbitrage trap, and it is closing.

Now the machine. The machine scales the other way entirely. You build the network once, and it serves the ten-thousandth customer at almost zero marginal cost. It works at three in the morning. It never turns over. It never calls in sick.

Remote video monitoring is that machine. Modern AI-edge analytics filter out roughly 99% of nuisance events — animals, shadows, headlights — before a human ever looks. That filtering is what lets a single trained operator monitor on the order of 500 cameras instead of 50.

In guarding, labor is the product. In RVM, labor supervises the product.

That one word — supervises — is the entire game.

Key Insight — Inversion. Charlie Munger's favorite move is to flip the question. Don't ask how to grow your guard company. Ask what would guarantee it is worth less in five years. Stay 100% labor-as-product. Carry no recurring revenue. Let one or two accounts dominate the book. Keep every relationship in your own head. Avoid that list and you have a strategy.

The Machine Didn't Sleep, Didn't Quit, and Didn't Need a Branch.

The ATM's real magic was never speed. It was that it broke banking free of the building.

Suddenly a customer could get their cash in a city where their bank owned no branch at all. Then online banking finished the job, and the bank moved into your pocket. The service became unbound from any particular piece of real estate.

Remote video monitoring has the same gift. It is geographically unbound. A Security Operations Center in Phoenix can watch a high-value property in Maine without a single truck or minute of drive time. It trades payroll for capital expenditure — you invest up front in cameras, telemetry, software, and the build-out of the SOC, and then you harvest a recurring stream for years.

That recurring stream is the part buyers actually fall in love with. Recurring monthly revenue, under contract, predictable. And it arrives with a hard-dollar story for the customer: false alarms make up an estimated 90% to 99% of all alarm calls and cost emergency services on the order of $1.8 billion a year, while verified video response has been shown to cut false dispatches by around 95%. That is not a feature. That is an argument that wins contracts and defends pricing.

Now hold both models in your head at once, because this is the part most owners miss.

Every wage hike. Every turnover spike. Every SCA bump. Read first-order, each one is simply "my costs went up." Read second-order, each one is also widening the advantage of the model where labor is a fraction of the cost stack instead of the whole thing. The same pressure that squeezed the teller window out of the branch is the pressure that made the machine look like genius.

Why this matters if you own a guard company: you are not just running a business with a margin problem. You are running the prior model in an industry visibly building the next one. The macro forces grinding on your P&L are the same forces re-rating the company across town that already made the jump.

Key Insight — Second-Order Thinking. The first-order reading of rising labor cost is pain. The second-order reading is a signal: the ground under the labor model is moving, and it is moving in the exact direction of remote monitoring. The owners who read it only first-order are the ones who get surprised.

The Market Stopped Paying for Branches. It Started Paying for the Platform.

Let's talk about your number.

A medium-sized manned guarding company typically changes hands somewhere around 6x to 7x EBITDA. A smaller, owner-dependent guard book often less — call it 4x to 5x. Meanwhile a platform-ready security business, the kind with a real management team, clean books, and 30% or more of revenue recurring, commands 7x to 10x and up.

That spread is not an accident. It is the market pricing two different machines.

The same thing happened in banking. The market quietly stopped rewarding branch count and started rewarding the low-cost, scalable platform. A branch full of tellers turned from an asset into a cost center. The franchise, the deposit base, the technology layer — that became the value.

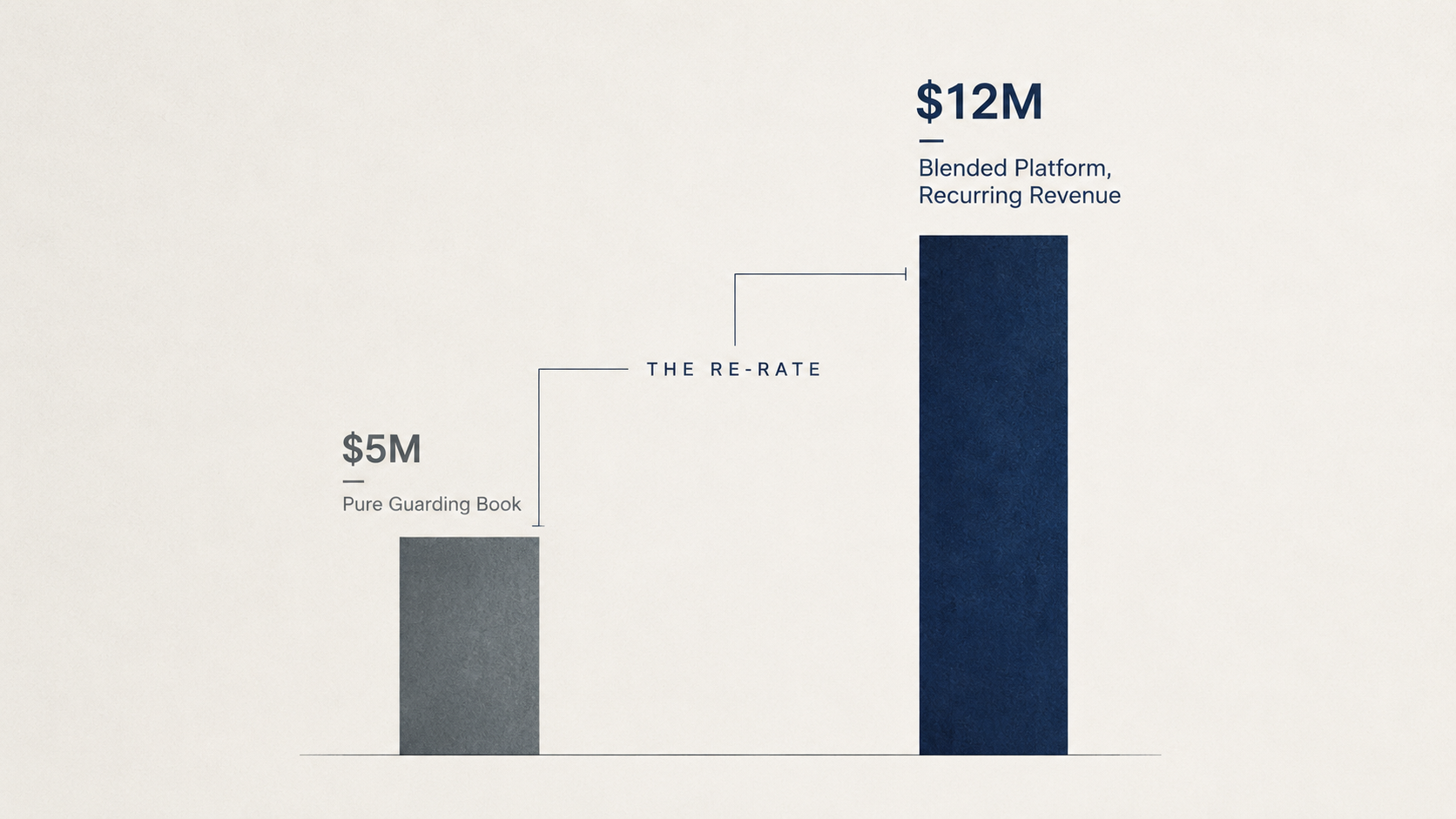

Let me show you what that re-rate does, with an illustrative example. And I mean illustrative — your number depends on your book.

Take a guard company doing $10 million in revenue at a 10% margin. That's $1 million of EBITDA. At 5x, the business is worth about $5 million.

Now run the same company three years forward, after the owner deliberately builds a remote monitoring line. Guarding is $9 million at 10%, so $900,000. The new RVM revenue is $2 million at roughly a 35% margin, so $700,000. Total EBITDA is about $1.6 million — and the company is no longer a pure guard book. It is a platform-ready story with real recurring revenue, and it earns a blended multiple closer to 7.5x.

That's roughly $12 million.

Revenue grew 10%. The value more than doubled — from about $5 million to about $12 million.

The gap between those two numbers is not the revenue. It is the re-rate — the market paying a higher multiple for a higher-quality stream of earnings. The teller never knew the branch's value was quietly moving from the lobby to the platform. Don't be the teller.

Key Insight — Map vs. Territory. EBITDA is the map. The quality of that EBITDA — how recurring it is, how contracted, how independent of you personally — is the territory. Two companies with identical EBITDA can be worth double or half of each other. Buyers underwrite the territory. Make sure that's what you're selling them.

Most Banks Didn't Build the App. They Sold the Branches.

Here is the part of the banking story that matters most to you.

When the machine changed the economics, the thousands of small community banks did not all rush off to build digital platforms. Most of them couldn't. Wrong capital, wrong scale, wrong stage of life for the people who owned them.

So look at what actually happened. The United States had more than 14,000 banks in the mid-1980s. Today it has fewer than 5,000.

Where did the other nine thousand go? They sold. They merged into acquirers who already had the platform, the technology, and the scale. And here is the part nobody puts on a slide: the owners who sold well — early, deliberately, into a strong market — captured real value for everything they had built. The ones who waited too long got acquired cheap, on someone else's terms, or simply faded.

You have three honest moves. I'll be direct about each, and I'll give you my odds.

You can convert — rebuild the company around remote monitoring yourself. Highest ceiling on value, highest execution risk. It needs capital, a real seven-to-ten-year runway, and a skill set most guard owners have to hire. Done well, I'd put it at maybe a 65% to 70% chance of a materially better exit. But "done well" is the entire sentence. A botched conversion destroys value faster than standing still.

You can blend — keep the guard book and layer a monitoring line on top, often starting with your own customers, then sell the combined platform-ready story. Slower re-rate, far smaller downside. For most established owners this is the best risk-adjusted path — I'd call it 60% to 65% odds of a real multiple lift, and it's where I'd point most people first.

Or you can sell into a platform — hand the business to an acquirer who already owns the machine, the SOC, the integration playbook, and let them run the conversion. You capture a fair number now and, structured right, rollover equity that pays you a second time when the larger platform sells. For an owner past 60 without an obvious successor or appetite for a capex cycle, this is, in my honest opinion, the highest expected value of the three.

Because here is the other side of that bet. The owner who picks "wait and do nothing" as a pure guard book is, in my estimate, carrying something like a 60% to 70% chance of selling into a flat or compressed multiple five years from now — because the buyer pool is increasingly underwriting RVM-convertible revenue, not labor hours.

Key Insight — Probabilistic Thinking. Don't ask which path is "right." Ask what the range of outcomes is for each, and how likely each one is. Then notice that two of the three paths — blend and sell — let someone else carry the execution risk while you still capture the upside. For an owner whose net worth is locked inside one illiquid company, that is not timidity. That is sound portfolio thinking.

The Lobby Is Still Busy. That's the Trap.

Let me name the reason most owners will read this, nod, and do nothing.

The lobby is still busy.

Right now, today, guarding still works. The contracts still renew. The invoices still get paid. Cash still lands on Friday. Customers still walk in the door. Nothing about today feels like an emergency, and so the decision slides to next year, and the year after that.

That is exactly how it went in banking.

The branch did not empty out in a season. For a long stretch it stayed busy, and busy felt like fine. Meanwhile the economics shifted underneath the floor — every year the machine took a little more, until one year the branch was a cost to be closed rather than an asset to be valued. The change was gradual. Then it was total. And by then there was no good buyer for a building full of teller windows.

The security M&A window, by contrast, is wide open today. Sector deal volume rose roughly 24% year over year in 2025. Well-capitalized platforms are completing dozens of acquisitions a year. A deep, hungry buyer pool is a genuine gift to a seller — but it is a gift with an expiration date, and it only pays the owner whose company is actually ready to be bought.

What if you wait? Then you are betting the lobby stays busy long enough. Maybe it does. But that is the one variable you do not control.

Key Insight — Asymmetric Risk. The cost of acting a year early is small — you sell into a strong market a little sooner than you had to. The cost of acting a year late is a structural re-rate you cannot undo. When the downside is that lopsided, you do not wait for certainty. You move while you still set the terms.

Look Past the Lobby.

Strip the story down and here is all of it.

The product is permanent. The machine changed. Guarding is the teller window — a labor business fighting a structural headwind. Remote video monitoring is the machine in the wall — a leverage business with recurring revenue, expanding margins, and a buyer pool that pays a premium for exactly those traits. The value of your company now depends almost entirely on which one a buyer believes they are getting.

You do not have to build the machine yourself. Plenty of great outcomes don't require it.

But you do have to decide. Because not deciding is itself a decision — it is the one that quietly reprices your company while you stand in a busy lobby telling yourself the windows have always had a line.

If you own a security company and you want an honest, confidential read on where you sit on this curve — what the business is worth today, and which of the three moves actually fits your timeline — that is the conversation NextGen Live Security exists to have. We are a HoldCo built to partner with founder-led security businesses. We keep the name you built and the team that built it with you, and we bring the machine: the technology, the operating system, and the capital that turns a regional book into a platform asset.

The teller never saw the machine coming.

You already have. So look past the lobby — and decide what your life's work is worth before someone else decides it for you.

Redefine Success

It All Begins Here

Confidence doesn’t always arrive with a bold entrance. Sometimes, it builds quietly, step by step, as we show up for ourselves day after day. It grows when we choose to try, even when we’re unsure of the outcome. Every time you take action despite self-doubt, you reinforce the belief that you’re capable. Confidence isn’t about having all the answers — it’s about trusting that you can figure it out along the way.

The key to making things happen isn’t waiting for the perfect moment; it’s starting with what you have, where you are. Big goals can feel overwhelming when viewed all at once, but momentum builds through small, consistent action. Whether you’re working toward a personal milestone or a professional dream, progress comes from showing up — not perfectly, but persistently. Action creates clarity, and over time, those steps forward add up to something real.

You don’t need to be fearless to reach your goals, you just need to be willing. Willing to try, willing to learn, and willing to believe that you’re capable of more than you know. The road may not always be smooth, but growth rarely is. What matters most is that you keep going, keep learning, and keep believing in the version of yourself you’re becoming.

Small Steps Create Big Shifts

It All Begins Here

Confidence doesn’t always arrive with a bold entrance. Sometimes, it builds quietly, step by step, as we show up for ourselves day after day. It grows when we choose to try, even when we’re unsure of the outcome. Every time you take action despite self-doubt, you reinforce the belief that you’re capable. Confidence isn’t about having all the answers — it’s about trusting that you can figure it out along the way.

The key to making things happen isn’t waiting for the perfect moment; it’s starting with what you have, where you are. Big goals can feel overwhelming when viewed all at once, but momentum builds through small, consistent action. Whether you’re working toward a personal milestone or a professional dream, progress comes from showing up — not perfectly, but persistently. Action creates clarity, and over time, those steps forward add up to something real.

You don’t need to be fearless to reach your goals, you just need to be willing. Willing to try, willing to learn, and willing to believe that you’re capable of more than you know. The road may not always be smooth, but growth rarely is. What matters most is that you keep going, keep learning, and keep believing in the version of yourself you’re becoming.

Turn Intention Into Action

It All Begins Here

Confidence doesn’t always arrive with a bold entrance. Sometimes, it builds quietly, step by step, as we show up for ourselves day after day. It grows when we choose to try, even when we’re unsure of the outcome. Every time you take action despite self-doubt, you reinforce the belief that you’re capable. Confidence isn’t about having all the answers — it’s about trusting that you can figure it out along the way.

The key to making things happen isn’t waiting for the perfect moment; it’s starting with what you have, where you are. Big goals can feel overwhelming when viewed all at once, but momentum builds through small, consistent action. Whether you’re working toward a personal milestone or a professional dream, progress comes from showing up — not perfectly, but persistently. Action creates clarity, and over time, those steps forward add up to something real.

You don’t need to be fearless to reach your goals, you just need to be willing. Willing to try, willing to learn, and willing to believe that you’re capable of more than you know. The road may not always be smooth, but growth rarely is. What matters most is that you keep going, keep learning, and keep believing in the version of yourself you’re becoming.

Make Room for Growth

It All Begins Here

Confidence doesn’t always arrive with a bold entrance. Sometimes, it builds quietly, step by step, as we show up for ourselves day after day. It grows when we choose to try, even when we’re unsure of the outcome. Every time you take action despite self-doubt, you reinforce the belief that you’re capable. Confidence isn’t about having all the answers — it’s about trusting that you can figure it out along the way.

The key to making things happen isn’t waiting for the perfect moment; it’s starting with what you have, where you are. Big goals can feel overwhelming when viewed all at once, but momentum builds through small, consistent action. Whether you’re working toward a personal milestone or a professional dream, progress comes from showing up — not perfectly, but persistently. Action creates clarity, and over time, those steps forward add up to something real.

You don’t need to be fearless to reach your goals, you just need to be willing. Willing to try, willing to learn, and willing to believe that you’re capable of more than you know. The road may not always be smooth, but growth rarely is. What matters most is that you keep going, keep learning, and keep believing in the version of yourself you’re becoming.