Remote Video Monitoring vs. Guards: Owner's Guide

The Machine in the Wall: What the Bank Teller Knows About Your Guard Company

Nobody mourns the bank teller. Banking didn't die when the machine arrived — it grew bigger, earned more, and became worth far more. It simply stopped running on people behind counters. If you own a security guard company, that is the most important story you are not thinking about.

I've been thinking about bank tellers.

Not the people. The job. Picture a bank in 1975. A lobby. A long counter. A row of windows, and behind each window a teller, counting cash by hand, one customer at a time. The bank's entire capacity to serve its town came down to a simple piece of arithmetic: how many windows were open, times how fast each teller could work.

Then somebody put a machine in the wall.

When the ATM arrived, everyone assumed it would gut the workforce and hollow out the banks. It did the opposite. Banking didn't shrink. It exploded. Banks served more customers, in more places, and made more money doing it. The machine — not the teller — became the engine. And the teller window quietly stopped being where the value lived.

I run NextGen Live Security, a HoldCo building a platform in remote video monitoring and live guarding. So I don't read the story of the bank teller as nostalgia. I read it as a forecast. Because if you own a security guard company, you are running a lobby full of teller windows.

And the machine is already in the wall.

This is for the owner who built something real — a guard company, an alarm book, a monitoring operation — over 20 or 30 years, and wants a clear-eyed answer before they exit. Not a panic. The math.

Here's the memo.

The Bank Never Sold Cash. It Sold Trust.

The teller slid you a stack of twenties, but cash was never the product.

The product was trust. Trust that your money was safe, accounted for, and there when you reached for it. The teller was just the delivery mechanism — a human face on a promise.

Sound familiar?

You have never sold guards. You sell what a guard delivers — the parking lot that stays empty, the construction site that still has its copper at sunrise, the night a business owner finally sleeps because somebody is watching. Pinkerton branded that promise in 1850 with an unblinking eye and three words: We Never Sleep. You sell the exact same thing today.

The product has not changed in 175 years.

What changed in banking was never the product. It was the machine underneath it. A teller window and an ATM deliver the identical promise. But one of them costs a salary every two weeks, turns over, trains slowly, and calls in sick. The other one does not.

Why this matters if you own a guard company: manned guarding is the teller window. Remote video monitoring is the machine in the wall. Same product — security, the end of uncertainty — built on two completely different cost structures. And the market has started paying very different prices for each.

Key Insight — First Principles. Strip the business to its core and the product is permanent: the end of the uncertainty that keeps your customer awake. Everything above that — the uniform, the truck, the teller window, the camera — is just machinery, and machinery gets replaced. The owners who fall in love with the machinery instead of the product tend to get replaced along with it.

One Teller Serves One Customer. The Machine Serves Ten Thousand.

Here is the hard ceiling of the teller window. It scales in exactly one direction: more people.

More customers means more windows, more tellers, more salaries, more turnover to manage. The teller is the capacity. The only operating leverage a branch manager ever had was orchestration — squeezing a little more throughput out of the people already on the payroll.

Guarding is identical. It scales linearly with human bodies. One post, one officer, every shift, forever. Your leverage is scheduling discipline, overtime control, route density. Real skill. Also a game with a hard ceiling, because the labor is the product.

And that labor gets more expensive and harder to hold every single year.

Contract security ran roughly 77% annual turnover in 2024, up from about 69% in 2019. Plenty of individual firms run 100% to 300% — they replace their entire workforce inside a year. More than 60% of security firms name rising hourly pay as their top turnover driver, and yet the median guard still earns around $38,000, a wage that has barely moved in real terms in two decades. You are paying more, and your officers still feel underpaid. In 2025 the Department of Labor pushed the Service Contract Act health-and-welfare fringe to $5.55 an hour — a hard, non-negotiable add to every billable hour on covered work.

That is the labor-arbitrage trap, and it is closing.

Now the machine. The machine scales the other way entirely. You build the network once, and it serves the ten-thousandth customer at almost zero marginal cost. It works at three in the morning. It never turns over. It never calls in sick.

Remote video monitoring is that machine. Modern AI-edge analytics filter out roughly 99% of nuisance events — animals, shadows, headlights — before a human ever looks. That filtering is what lets a single trained operator monitor on the order of 500 cameras instead of 50.

In guarding, labor is the product. In RVM, labor supervises the product.

That one word — supervises — is the entire game.

Key Insight — Inversion. Charlie Munger's favorite move is to flip the question. Don't ask how to grow your guard company. Ask what would guarantee it is worth less in five years. Stay 100% labor-as-product. Carry no recurring revenue. Let one or two accounts dominate the book. Keep every relationship in your own head. Avoid that list and you have a strategy.

The Machine Didn't Sleep, Didn't Quit, and Didn't Need a Branch.

The ATM's real magic was never speed. It was that it broke banking free of the building.

Suddenly a customer could get their cash in a city where their bank owned no branch at all. Then online banking finished the job, and the bank moved into your pocket. The service became unbound from any particular piece of real estate.

Remote video monitoring has the same gift. It is geographically unbound. A Security Operations Center in Phoenix can watch a high-value property in Maine without a single truck or minute of drive time. It trades payroll for capital expenditure — you invest up front in cameras, telemetry, software, and the build-out of the SOC, and then you harvest a recurring stream for years.

That recurring stream is the part buyers actually fall in love with. Recurring monthly revenue, under contract, predictable. And it arrives with a hard-dollar story for the customer: false alarms make up an estimated 90% to 99% of all alarm calls and cost emergency services on the order of $1.8 billion a year, while verified video response has been shown to cut false dispatches by around 95%. That is not a feature. That is an argument that wins contracts and defends pricing.

Now hold both models in your head at once, because this is the part most owners miss.

Every wage hike. Every turnover spike. Every SCA bump. Read first-order, each one is simply "my costs went up." Read second-order, each one is also widening the advantage of the model where labor is a fraction of the cost stack instead of the whole thing. The same pressure that squeezed the teller window out of the branch is the pressure that made the machine look like genius.

Why this matters if you own a guard company: you are not just running a business with a margin problem. You are running the prior model in an industry visibly building the next one. The macro forces grinding on your P&L are the same forces re-rating the company across town that already made the jump.

Key Insight — Second-Order Thinking. The first-order reading of rising labor cost is pain. The second-order reading is a signal: the ground under the labor model is moving, and it is moving in the exact direction of remote monitoring. The owners who read it only first-order are the ones who get surprised.

The Market Stopped Paying for Branches. It Started Paying for the Platform.

Let's talk about your number.

A medium-sized manned guarding company typically changes hands somewhere around 6x to 7x EBITDA. A smaller, owner-dependent guard book often less — call it 4x to 5x. Meanwhile a platform-ready security business, the kind with a real management team, clean books, and 30% or more of revenue recurring, commands 7x to 10x and up.

That spread is not an accident. It is the market pricing two different machines.

The same thing happened in banking. The market quietly stopped rewarding branch count and started rewarding the low-cost, scalable platform. A branch full of tellers turned from an asset into a cost center. The franchise, the deposit base, the technology layer — that became the value.

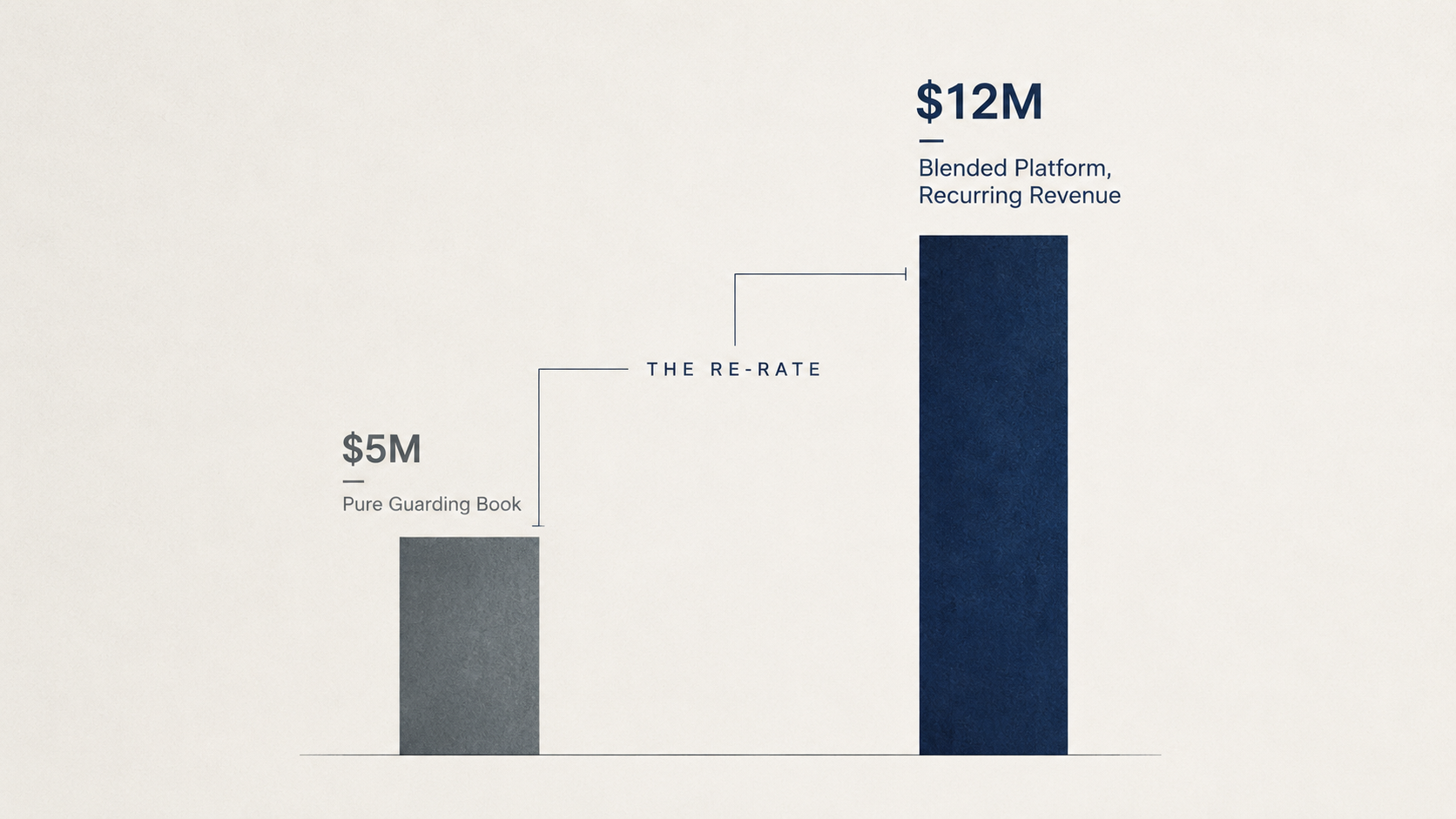

Let me show you what that re-rate does, with an illustrative example. And I mean illustrative — your number depends on your book.

Take a guard company doing $10 million in revenue at a 10% margin. That's $1 million of EBITDA. At 5x, the business is worth about $5 million.

Now run the same company three years forward, after the owner deliberately builds a remote monitoring line. Guarding is $9 million at 10%, so $900,000. The new RVM revenue is $2 million at roughly a 35% margin, so $700,000. Total EBITDA is about $1.6 million — and the company is no longer a pure guard book. It is a platform-ready story with real recurring revenue, and it earns a blended multiple closer to 7.5x.

That's roughly $12 million.

Revenue grew 10%. The value more than doubled — from about $5 million to about $12 million.

The gap between those two numbers is not the revenue. It is the re-rate — the market paying a higher multiple for a higher-quality stream of earnings. The teller never knew the branch's value was quietly moving from the lobby to the platform. Don't be the teller.

Key Insight — Map vs. Territory. EBITDA is the map. The quality of that EBITDA — how recurring it is, how contracted, how independent of you personally — is the territory. Two companies with identical EBITDA can be worth double or half of each other. Buyers underwrite the territory. Make sure that's what you're selling them.

Most Banks Didn't Build the App. They Sold the Branches.

Here is the part of the banking story that matters most to you.

When the machine changed the economics, the thousands of small community banks did not all rush off to build digital platforms. Most of them couldn't. Wrong capital, wrong scale, wrong stage of life for the people who owned them.

So look at what actually happened. The United States had more than 14,000 banks in the mid-1980s. Today it has fewer than 5,000.

Where did the other nine thousand go? They sold. They merged into acquirers who already had the platform, the technology, and the scale. And here is the part nobody puts on a slide: the owners who sold well — early, deliberately, into a strong market — captured real value for everything they had built. The ones who waited too long got acquired cheap, on someone else's terms, or simply faded.

You have three honest moves. I'll be direct about each, and I'll give you my odds.

You can convert — rebuild the company around remote monitoring yourself. Highest ceiling on value, highest execution risk. It needs capital, a real seven-to-ten-year runway, and a skill set most guard owners have to hire. Done well, I'd put it at maybe a 65% to 70% chance of a materially better exit. But "done well" is the entire sentence. A botched conversion destroys value faster than standing still.

You can blend — keep the guard book and layer a monitoring line on top, often starting with your own customers, then sell the combined platform-ready story. Slower re-rate, far smaller downside. For most established owners this is the best risk-adjusted path — I'd call it 60% to 65% odds of a real multiple lift, and it's where I'd point most people first.

Or you can sell into a platform — hand the business to an acquirer who already owns the machine, the SOC, the integration playbook, and let them run the conversion. You capture a fair number now and, structured right, rollover equity that pays you a second time when the larger platform sells. For an owner past 60 without an obvious successor or appetite for a capex cycle, this is, in my honest opinion, the highest expected value of the three.

Because here is the other side of that bet. The owner who picks "wait and do nothing" as a pure guard book is, in my estimate, carrying something like a 60% to 70% chance of selling into a flat or compressed multiple five years from now — because the buyer pool is increasingly underwriting RVM-convertible revenue, not labor hours.

Key Insight — Probabilistic Thinking. Don't ask which path is "right." Ask what the range of outcomes is for each, and how likely each one is. Then notice that two of the three paths — blend and sell — let someone else carry the execution risk while you still capture the upside. For an owner whose net worth is locked inside one illiquid company, that is not timidity. That is sound portfolio thinking.

The Lobby Is Still Busy. That's the Trap.

Let me name the reason most owners will read this, nod, and do nothing.

The lobby is still busy.

Right now, today, guarding still works. The contracts still renew. The invoices still get paid. Cash still lands on Friday. Customers still walk in the door. Nothing about today feels like an emergency, and so the decision slides to next year, and the year after that.

That is exactly how it went in banking.

The branch did not empty out in a season. For a long stretch it stayed busy, and busy felt like fine. Meanwhile the economics shifted underneath the floor — every year the machine took a little more, until one year the branch was a cost to be closed rather than an asset to be valued. The change was gradual. Then it was total. And by then there was no good buyer for a building full of teller windows.

The security M&A window, by contrast, is wide open today. Sector deal volume rose roughly 24% year over year in 2025. Well-capitalized platforms are completing dozens of acquisitions a year. A deep, hungry buyer pool is a genuine gift to a seller — but it is a gift with an expiration date, and it only pays the owner whose company is actually ready to be bought.

What if you wait? Then you are betting the lobby stays busy long enough. Maybe it does. But that is the one variable you do not control.

Key Insight — Asymmetric Risk. The cost of acting a year early is small — you sell into a strong market a little sooner than you had to. The cost of acting a year late is a structural re-rate you cannot undo. When the downside is that lopsided, you do not wait for certainty. You move while you still set the terms.

Look Past the Lobby.

Strip the story down and here is all of it.

The product is permanent. The machine changed. Guarding is the teller window — a labor business fighting a structural headwind. Remote video monitoring is the machine in the wall — a leverage business with recurring revenue, expanding margins, and a buyer pool that pays a premium for exactly those traits. The value of your company now depends almost entirely on which one a buyer believes they are getting.

You do not have to build the machine yourself. Plenty of great outcomes don't require it.

But you do have to decide. Because not deciding is itself a decision — it is the one that quietly reprices your company while you stand in a busy lobby telling yourself the windows have always had a line.

If you own a security company and you want an honest, confidential read on where you sit on this curve — what the business is worth today, and which of the three moves actually fits your timeline — that is the conversation NextGen Live Security exists to have. We are a HoldCo built to partner with founder-led security businesses. We keep the name you built and the team that built it with you, and we bring the machine: the technology, the operating system, and the capital that turns a regional book into a platform asset.

The teller never saw the machine coming.

You already have. So look past the lobby — and decide what your life's work is worth before someone else decides it for you.